Spoiler Alert – You should have at least ₹ 2.25 Crores if you want to retire in India. To know why and how read further.

There are many decisions you need to make when you retire as a non-resident Indian (NRI). If you want this dream to come true, it is important that you think about your finances.

When you think of “crorepati,” you might think of someone who has a lot of money, but that doesn’t mean they can retire comfortably.

In terms of retirement planning, there are two main things to do: save as much as you can and invest as much as you can.

But the amount of money you’ll need to retire comfortably depends on your expenses, your lifestyle, and your own financial goals, so it’s important to figure out how much money you’ll need.

So taking a big picture look at your retirement can help you figure out how much money you should save.

FAQ #1: How much should I save for retirement?

To start with, you need to know how much money you will need when you retire to live a good life.

This depends on two things: when you’re going to retire, and how much money you’ll need each month after you retire.

Case Study #1:

Let’s think about these assumptions:

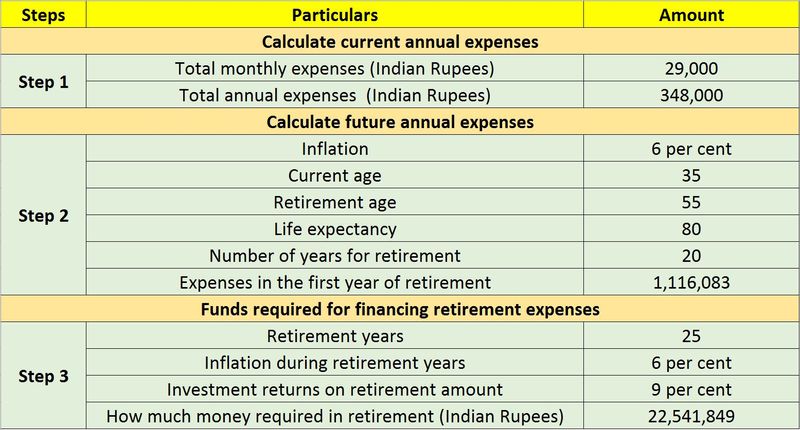

- Current age: 35 years

- Monthly expenses: ₹29,000

- Inflation considered: 6 per cent

- Retirement age considered: 55 years

- How much you may live post-retirement: 80 years

Here’s how you get to the amount you’re going to need:

The cost table for NRIs

It’s important to figure out how much money you should save for your retirement.

Step-by-step: How do I figure out how much I spend each year and in the future?

At the beginning, you need to know how much you spend each year: Let’s say that your monthly expenses are Rs29,000, and your annual expenses come out to ₹ 348,000, which is how much you spend each year (i.e. ₹ 29,000 multiplied by 12)

The second thing to do is figure out how much money you’ll need in the future to buy things. At a 6% rate of inflation, your annual expenses after you retire will be ₹11 Lakhs per year, each year.

Finally, we have worked out how much money you will need to cover your retirement costs after you retire:

The average life expectancy for a person is 80 years. If we assume that your retirement age is 55 and that your life expectancy is 80 years, we will say that you will have 25 years after you retire.

It also works this way: If you invest your retirement money in a safe or traditional product that earns you 9 per cent a year and inflation stays the same, you’ll get about 3 per cent in net interest every year.

With the calculations above in mind, you will need a corpus (the total money you invest) of ₹ 2.25 Crores to start your business.

First, this may seem like a lot of money. But for people who plan ahead, it’s possible. As long as your goal is at least 20 years away, start a regular investment plan (SIP or systematic investment plan) in a mutual fund to save for your retirement and you’re all set!

FAQ #2: What if I don’t have that many years until retirement?

So let’s say that you don’t have a lot of money saved up for retirement yet, but you have about ₹ 1 Crores in savings now. Let’s look at what you can do.

Case Study #2:

Let’s think about these assumptions:

- Current age: 50 years

- Current savings: ₹ 1 Crore

- Investment rate of return: 10 per cent to 12 per cent

- Retirement age considered: 60 years

- How much you may live post-retirement: 80 years

There is a 50-year-old NRI who has a starting fund of Rs10 million. By the time he or she is 60, someone needs a compounded annual growth rate (CAGR) of 20% to grow from ₹ 1 crore to ₹ 6 crores in 10 years (19.62 per cent, to be precise).

If you want to make money, you can’t expect to make money at a rate of 20%. This corpus isn’t enough to make the needed one.

If the starting corpus was bigger, like ₹ 2 Crore to ₹ 2.5 Crores, it would grow to Rs. 6 Crores at a rate of 9 per cent to 12 per cent per year (9.15 per cent to 11.62 per cent to be precise).

If most of the money in the fund was invested in stocks, this rate of return looks reasonable and possible.

With a start-up fund of Rs. 1 Crore, the NRI can still build up enough money to meet his needs. He’ll have to make a lot of contributions over the next 10 years.

People who have a lot of money can start making regular investments in the fund on a regular basis. To get the required corpus, the investment plan amount would need to be between ₹ 1,00,000 and ₹ 1,50,000 a month. This is based on a 10% to 12% rate of return over the time frame.

People can’t say for sure which asset class will make money for them in the future when they invest for long periods of time.

There are two ways a 50-year-old NRI can start: with a corpus of ₹ 2.5 Crores or with a corpus of ₹ 1 crore and a monthly investment of up to₹ 1,50,000 (equities).

FAQ #3: What if I keep investing in safe investments?

Suppose your risk tolerance is low, and you can’t afford to invest in the stock market. Instead, you prefer to invest in “fixed income” investments, which are thought to be the safest way to invest money, but they can lose money. Let’s look at what you can do.

WHAT ARE FIXED INCOME INSTRUMENTS?

Fixed income instruments are types of financial instruments that guarantee a certain amount of money back and protect your money. For example, they aren’t afraid of changes in the market and have a fixed rate of interest for the whole time you invest.

There are many types of fixed-income products, like government or treasury bonds and bills, municipal bonds, corporate bonds, and certificates of deposit (CDs).

As a reward, the issuing bank pays interest on the amount of money that is in the account for a set amount of time. This could be for six months, a year, or five years. People who buy CDs get back the money they put in, as well as any interest that they earned.

Case Study #3:

- Current age: 50 years

- Current savings: ₹ 2.5 Crores

- Investment rate of return: 4 per cent

- Retirement age considered: 60 years

- How much you may live post-retirement: 95 years

In 10 years, if you had about ₹ 2.5 Crores and invested it in fixed income products that earned 4% net of taxes in India, you would have about ₹ 3.7 Crores in your bank account.

It would be enough to spend about ₹ 25,000 a month (or ₹ 3,00,000 a year) if you already own a house and you don’t want your money to run out at 85 or 90.

Financial planners say it’s possible to live in India with that amount of money, even though most people think it isn’t possible, too. It is just a more basic way of life.

In 10 years, if you have Rs. 1 Crore and only invest in fixed-income investments, you will have ₹ 1.5 Crores in your account. In India, if you live on ₹ 25,000 a month, this could last you for about 20 years.

After that, you won’t have any more money. What you can do to get out of this situation is to save more of your income for the last few years of your work, retire later, cut back on post-retirement spending, learn how to take risks, and invest in stocks.

The Main Things to Remember From the Above Three Case Studies:

- It doesn’t matter if the person is in the first case study or the second one. If they don’t already have a lot of risk tolerance, they need to learn how to build it.

- People who are retiring in a few years will need to be able to take risks for a few more decades. Even in retirement, the money they have will have to be invested in stocks.

- If the person can’t do that, he or she should get used to a much less affluent lifestyle in retirement, and their monthly contributions would also need to rise a lot.

- People would need a lot more money when they retire if their savings were only in fixed-income instruments.

- Risk tolerance: For this, experts say you should learn more about equities, how businesses make money, why investors follow herds in markets and what they do when they invest, among other things.

Donald G. is the Principal Consultant at NRI Money+. He specialises in creating personalised financial plans for NRIs (Non-Resident Indians) and HNI (High Net-worth Individuals).